April 2, 2021

The government should slash the onerous tax of 26-27% on non-life and agriculture insurance premium that blocks entry of cash-rich private sector investors that can significantly accelerate rural farm activity through financing.

The misery of Filipino farmers is often blamed on the dearth of facilities on micro-financing and its constant aid micro-insurance.

But agri-finance expert Dr. Jaime Aristotle Alip asserts in a webinar hosted by the Southeast Asian Regional Center for Graduate Study & Research in Agriculture (SEARCA) that cutting tax on insurance premium will significantly raise the number of private insurance offerings.

Alip is chairman emeritus and pioneering founder of the country’s largest microfinance firm CARD MRI (Center for Agriculture & Rural Development Inc.-Mutually Reinforcing Institutions).

He said tax on non-life insurance, including those for crop or agriculture insurance, should be around the rate of life insurance which is only at a minimal 2%. Other non-life insurance with high tax he cites are disaster insurance and health insurance.

“If you want private sector participation, you must level the playing field. You should lower down non-life premium tax (including tax for crop or agriculture insurance). I think there will be many private sector players (given this),” said Alip during SEARCA’s microinsurance forum.

SEARCA held the virtual forum “Agricultural Investment Risks: Empowering Smallholder Farmers through Micro-Insurance” as part of its thrust toward Accelerating Transformation Through Agricultural Innovation (ATTAIN).

Government does need to subsidize agri insurance because the regime will be market-driven.

“It will be the law of numbers and the law of efficiency (that will work). The gap must be addressed. Lawmakers should make non life insurance affordable,” Alip said.

Alip, a Ramon Magsaysay awardee (2008), stressed micro-insurance plays a significant role in boosting private sector investment in micro-financing or in extending loans to small farmers.

Once there is insurance or a guarantee program for farmers’ loans, banks are automatically willing to lend even to small farmers, Alip said.

CARD pays insurance claims fast — precisely because there has already been a pre-deposited insurance premium for the disaster, calamity, or typhoon.

“Within 8 hours we’ll pay. If there’s an issue (problems) involved, in 48 hours we will pay. The speed of payment shows how serious you are. Microinsurance should be believable. It should just be like a deposit when there’s a claim. You pay it right away,” he said.

Insurance or a loan guarantee is critically important in financing the marginalized farmers, in enabling them to get out of poverty.

If farmers are paid right away, they will be able to re-invest in agriculture again after a misfortune.

“Insurance is an important safety net so that the poor will not slide back to poverty. If we’re able to pay farmers right away, their loyalty and affinity to insurance will be there,” he said.

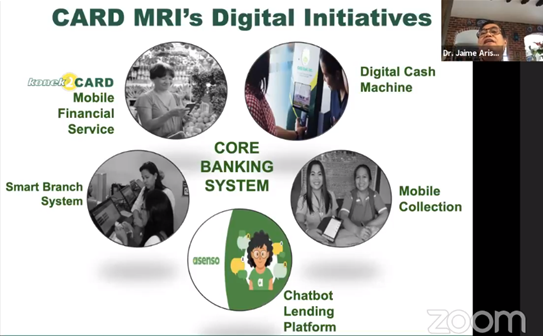

Because of digitization, CARD accelerated its payment systems. It now pays through mobile means (celfone).

With the Covid 19 pandemic’s lockdowns, its clients do not need to go to its offices. They can make payments, deposit, and withdraw online.

CARD was put up in December 1986. It has grown into a group of 23 mutually reinforcing institutions (MRI).

“My vision was for a bank owned and managed by the poor. I believe the reason why poor people are poor is not because of lack of access to resources. It is the lack of control over resources,” he said.

“After 10 years, we put up the first microfinance institution in the country, the CARD Bank, owned by its members. We completely turned banking system upside down.”

CARD Bank cut all bureaucracy in lending. It releases loans just two days from application.

It does not require collateral from borrowers.

Instead of requiring small borrowers financial projections or feasibility studies and numerous documents, it just requires a one-page form for loan application.

Now it has spin-off companies engaged in lending in both rural areas and urban areas.

It has the CARD MBA (mutual benefit association) owned by members and a non life insurance business linked with Pioneer Group

“All policies, all regulations within the standard of the Insrance Commission, are implemented by the owners. What is our value proposition for these companies? Since they own it, we have a very small premium,” he said.

Overhead cost of the company is only 1-2% while some insurance companies incur 40-60% overhead cost.

CARD now has 3,482 offices in 85 provinces covering 1,577 municipalities and cities and 40,440 barangays.

“The last frontier of the country is in Tawi Tawi, in Sitangkay. We are present there,–

30 minutes away from there by pumpboat, you are in Malaysia.”

It is in Balut Island in South Cotabato; 45 minutes to 1 hour from there, you are in Indonesia. It is also in Batanes, right near Taiwan.

It has 17,157 full-time staff. It has offices for OFWs (overseas Filipino workers) in HOngkong, Myanmar, Laos, Thailand, Cambodia, Indonesia, and Vietnam.

“This is how we are exporting the technology of CARD in micro-financing and micro-insurance.”

As of January 2021, it has so far served 7.43 million clients; insured 27.219 million individuals; has outstanding loan of P30.77 billion; savings of P28 billion; operational efficiency, 117.1%; financial sufficiency, 114.89%, number of stockholders, 120,252.

It accounts now for 20% percent of the entire microfinance industry in the country.

It has extended 14,761 scholarships; 9,783 graduate scholarships; and 4.693 million with access to its health services.

It accounts for around 80% of entire insured Filipinos. Those it insures are mostly in the poverty level who are given the chance to bounce back economically in times of difficulty and loss.

Its repayment rate before the pandemic was 99.9 percent. It faltered a bit due to the pandemic and is now recovering in repayment rate to a more stable 93-95%.

“ “We’re not just in the business of microfinance and imicroinsurance. Were in the business of poverty eradication,” said Alip. “Our major focus is on very poor women. If you’re able to help poor women to do business, their priority will always be the family, food for the children, education for the children.”

These are among its functions:

- It owns hospitals, clinics and keeps doctors and nurses. It has a pharmacy company that supports clients with affordable and generic medicine.

- It has a marketing support for farmers and businesses engaged in cottage products to help these expand and grow.

- It has a school on microfinance and microinsurance.

- It has health insurance and hospitalization insurance

- It has training programs and a school for college courses offering Entrepreneurship, Accountancy, Information Technology, and Tourism. (Melody Mendoza Aguiba)